Sustainability Measurement Standards

12/26/2022

The primary audience of this blog are the investors and anyone who is new to sustainable investing world.

Sustainability is the moral, social, and ethical responsibility of every human on this planet. Before discuss Sustainability Measurement Standards in detail, I would like to provide background of United Nations Organization and it is role in Sustainable Development Goals. Then comes the Sustainability Measurement standards which is very important to measure and monitor the progress and take corrective actions.

In 1945 towards the end of the world war II, the nations were in ruin and the world wanted peace. Representatives from 50 countries gathered, discussed and signed the UN charter giving birth to United Nations Organization with the hope to prevent another world war.

Presently, it is made f 193 Member States. It is one place on Earth where all the world's nations gather to discuss common problems, and recommend solutions that benefit all of humanity. The United Nations has evolved over the years to keep pace with a rapidly changing world. The UN has defined sustainable development goals for 2030, to achieve a better and more sustainable future for us all. UN Member States have also agreed to climate action to limit global warming.

Goal 1: No Poverty: Donate what you don't use

Goal 2: Zero Hunger: Waste less food and support local farmers

Goal 3: Good Health and Well Being: Vaccinate your family

Goal 4: Quality Education: Help Educate the Children in your community

Goal 5: Gender Equality: Empower women and girls and ensure their equal rights

Goal 6: Clean Water and Sanitation: Avoid wasting water

Goal 7: Affordable and Clean Energy: Use energy efficient appliances and light bulbs

Goal 8: Decent Work and Economic Growth: Create Job opportunities for youth

Goal 9: Industry, Innovation and Infrastructure: Fund the projects that provide basic infrastructure.

Goal 10: Reduced Inequalities: Support the marginalized or disadvantaged

Goal 11: Sustainable Cities and Communities: Bike, Walk or Use Public transportation.

Goal 12: Responsible consumption and production: Recycle paper, plastic, glass and aluminum.

Goal 13: Climate Action: Act Now to stop global warming

Goal 14: Life below water: Avoid plastic bags to keep water ocean clean

Goal 15: Life on Land: Plant a Tree and protect the environment

Goal 16: Peace, Justice and String Institution: StandUp for Human Rights

Goal 17: Partnerships: Lobby your government to boost development financing

Now we know that we have seventeen sustainable development goals along with the timeline of 2030. Now let's move onto implementation and enabling factors and accountability of the goals.

With the launch of the SDGs, the biggest challenge in implementing the SDGs is to raise funds. If $ 3 trillion to $ 4.5 trillion of an annual budget is required to fully implement the SDGs UN approaches the member countries for funding. However, National Assembly in many countries often rejected the promised budget to UN towards the SDGs. The reason is the priority of this budgets for an internal situation in the countries than towards the SDGs. This is why the participation of corporations is essential that directly influence the regions, classes, and gender in the financial aspect. Corporations build infrastructures around the world to make and distribute goods and services, which make an impact on both social and economical impact in the global environment. For effective participation of the corporates in the SDGs, an accurate analysis is required to determine how the corporation will participate in accordance with the characteristics of each entity. The association encourages many companies in various sectors to proactively respond to climate change, ethical issues, and social inequality.

Companies both in public and private sector contribute through their products and services offerings in the global or local environment leading to social and economic development aligned with the SDGs. Organizations now provide data that allows public investors to incorporate sustainability and impact considerations into their investment strategies.

Similar to financial accounting and reporting standards we have sustainability reporting and accounting standards.

The most common sustainability disclosure standards include:

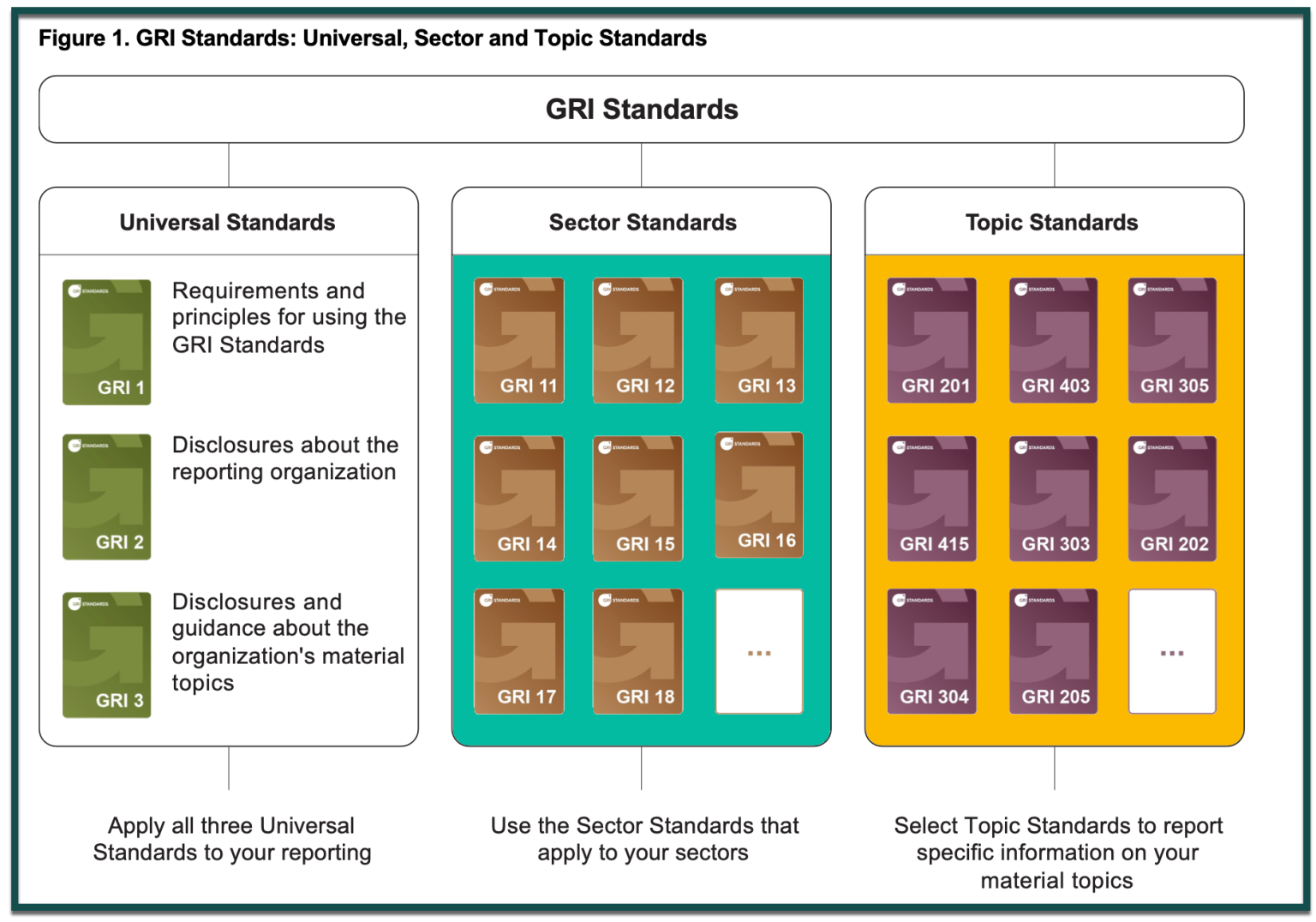

More information on the GRI standards can be found here.

Please note that some of the images and content shared on this page is referenced to the external sites, for example, https://www.globalreporting.org. The content is constantly evolving on these websites with the continuous improvement of the sustainability reporting standards.

The Sustainability Accounting Standards Board (SASB) is now part of the IFRS (International Financial Reporting System). ASB Standards are now under the oversight of the ISSB (International Sustainability Standard Board). The key words that are unique about the SASB are:

Financially Material: Firms should focus on report everything that could affect the financial performance of the company.

Industry-Based: Report issues that are industry based and are material to all its stake-holders.

Decision-Useful: Useful for investors in decision making.

Cost-Effective: SASB Standards are cost-effective for companies to use and share their SASB report

Evidence-Based & Market Informed: Information is presented or modeled after the accounting standards.

The question that may arise in your mind is, what standards am I suppose to follow with these three different standards listed above. The information appears to repeat at times among different reports. Is there specific guideline for me and my firm?

Well, I found a very valuable information on ESG Disclosure by PWC. Here is the link.

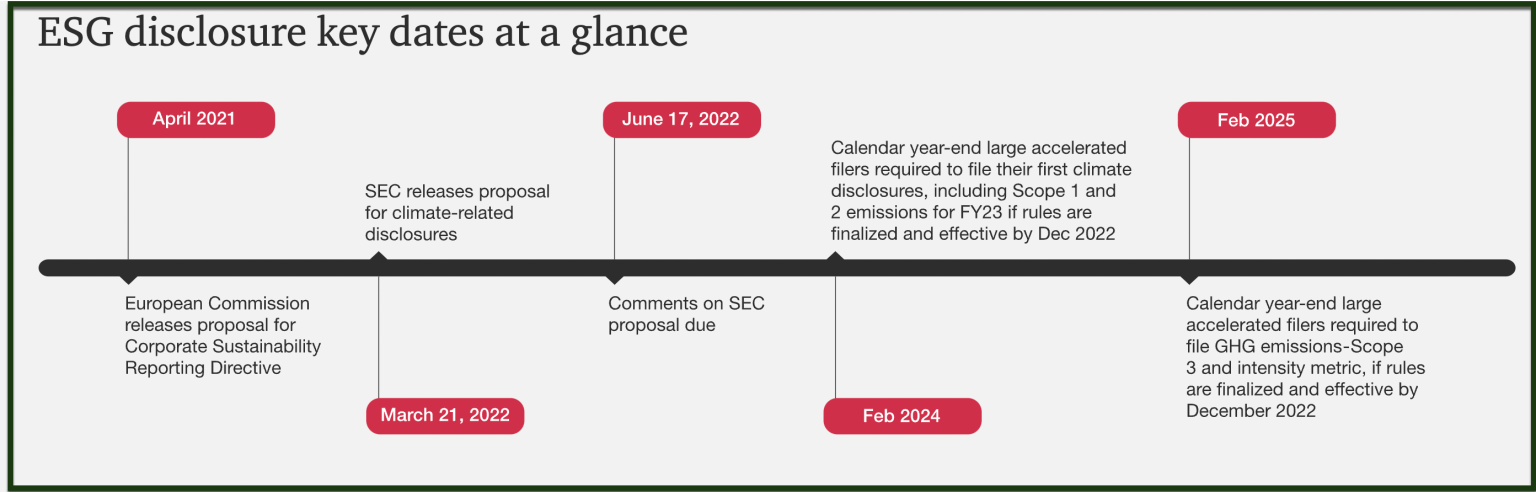

Also, here is the important timeline they have posted on their website.

In the US, the proposed disclosures are broadly aligned with frameworks such as the Task Force on Climate-Related Financial Disclosures (TCFD).

In the European Union and the US-based companies with entities there comply with the European Commission's Corporate Sustainability Reporting Directive (CSRD)

The ESG reporting standard work is in progress. The important steps being taken by the ISSB in developing consistent ESG reporting standards and strengthening capital markets.

Sustainability is the moral, social, and ethical responsibility of every human on this planet. Before discuss Sustainability Measurement Standards in detail, I would like to provide background of United Nations Organization and it is role in Sustainable Development Goals. Then comes the Sustainability Measurement standards which is very important to measure and monitor the progress and take corrective actions.

In 1945 towards the end of the world war II, the nations were in ruin and the world wanted peace. Representatives from 50 countries gathered, discussed and signed the UN charter giving birth to United Nations Organization with the hope to prevent another world war.

Presently, it is made f 193 Member States. It is one place on Earth where all the world's nations gather to discuss common problems, and recommend solutions that benefit all of humanity. The United Nations has evolved over the years to keep pace with a rapidly changing world. The UN has defined sustainable development goals for 2030, to achieve a better and more sustainable future for us all. UN Member States have also agreed to climate action to limit global warming.

Goal 1: No Poverty: Donate what you don't use

Goal 2: Zero Hunger: Waste less food and support local farmers

Goal 3: Good Health and Well Being: Vaccinate your family

Goal 4: Quality Education: Help Educate the Children in your community

Goal 5: Gender Equality: Empower women and girls and ensure their equal rights

Goal 6: Clean Water and Sanitation: Avoid wasting water

Goal 7: Affordable and Clean Energy: Use energy efficient appliances and light bulbs

Goal 8: Decent Work and Economic Growth: Create Job opportunities for youth

Goal 9: Industry, Innovation and Infrastructure: Fund the projects that provide basic infrastructure.

Goal 10: Reduced Inequalities: Support the marginalized or disadvantaged

Goal 11: Sustainable Cities and Communities: Bike, Walk or Use Public transportation.

Goal 12: Responsible consumption and production: Recycle paper, plastic, glass and aluminum.

Goal 13: Climate Action: Act Now to stop global warming

Goal 14: Life below water: Avoid plastic bags to keep water ocean clean

Goal 15: Life on Land: Plant a Tree and protect the environment

Goal 16: Peace, Justice and String Institution: StandUp for Human Rights

Goal 17: Partnerships: Lobby your government to boost development financing

Now we know that we have seventeen sustainable development goals along with the timeline of 2030. Now let's move onto implementation and enabling factors and accountability of the goals.

With the launch of the SDGs, the biggest challenge in implementing the SDGs is to raise funds. If $ 3 trillion to $ 4.5 trillion of an annual budget is required to fully implement the SDGs UN approaches the member countries for funding. However, National Assembly in many countries often rejected the promised budget to UN towards the SDGs. The reason is the priority of this budgets for an internal situation in the countries than towards the SDGs. This is why the participation of corporations is essential that directly influence the regions, classes, and gender in the financial aspect. Corporations build infrastructures around the world to make and distribute goods and services, which make an impact on both social and economical impact in the global environment. For effective participation of the corporates in the SDGs, an accurate analysis is required to determine how the corporation will participate in accordance with the characteristics of each entity. The association encourages many companies in various sectors to proactively respond to climate change, ethical issues, and social inequality.

Companies both in public and private sector contribute through their products and services offerings in the global or local environment leading to social and economic development aligned with the SDGs. Organizations now provide data that allows public investors to incorporate sustainability and impact considerations into their investment strategies.

Similar to financial accounting and reporting standards we have sustainability reporting and accounting standards.

The most common sustainability disclosure standards include:

- The Global Reporting Initiative (GRI): was the first set of sustainability standards globally launched in 1997. It provides guidelines for the disclosure of the non-financial sustainability reporting requirements on economic, environmental, and social performance areas.

- The Sustainability Accounting Standards Board (SASB): Launched in 2011, provides guidance on sector specific ESG topics. It develops reporting standards that track sustainability related metrics that are most financially material to their investors. According to SASB, firms should focus on reporting metrics that are material to their business.

- The Task Force on Climate-Related Financial Disclosures (TCFD): Launched in 2017, provides guidance to companies on disclosing climate-related risks, opportunities, and financial impacts to investors and other stakeholders. TCFD provides both general and sector-specific guidance on climate-related topics.

More information on the GRI standards can be found here.

Please note that some of the images and content shared on this page is referenced to the external sites, for example, https://www.globalreporting.org. The content is constantly evolving on these websites with the continuous improvement of the sustainability reporting standards.

The Sustainability Accounting Standards Board (SASB) is now part of the IFRS (International Financial Reporting System). ASB Standards are now under the oversight of the ISSB (International Sustainability Standard Board). The key words that are unique about the SASB are:

Financially Material: Firms should focus on report everything that could affect the financial performance of the company.

Industry-Based: Report issues that are industry based and are material to all its stake-holders.

Decision-Useful: Useful for investors in decision making.

Cost-Effective: SASB Standards are cost-effective for companies to use and share their SASB report

Evidence-Based & Market Informed: Information is presented or modeled after the accounting standards.

The question that may arise in your mind is, what standards am I suppose to follow with these three different standards listed above. The information appears to repeat at times among different reports. Is there specific guideline for me and my firm?

Well, I found a very valuable information on ESG Disclosure by PWC. Here is the link.

Also, here is the important timeline they have posted on their website.

In the US, the proposed disclosures are broadly aligned with frameworks such as the Task Force on Climate-Related Financial Disclosures (TCFD).

In the European Union and the US-based companies with entities there comply with the European Commission's Corporate Sustainability Reporting Directive (CSRD)

The ESG reporting standard work is in progress. The important steps being taken by the ISSB in developing consistent ESG reporting standards and strengthening capital markets.