Importance of Inventory in Investing Decisions

05/16/2023

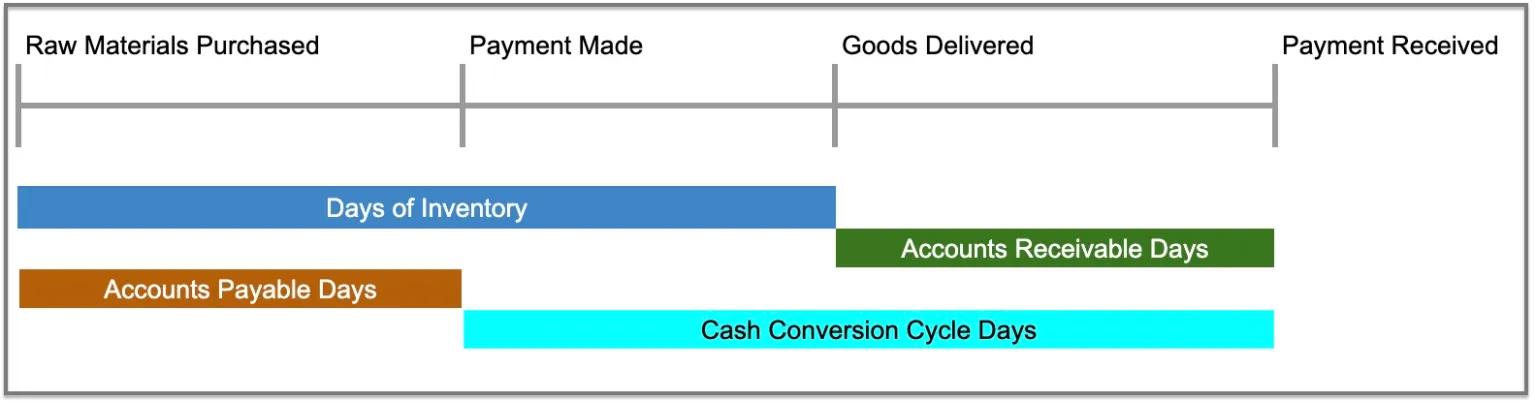

One of the reasons, an Investor wants to analyze the inventory ratios is to know the Cash Conversion Cycle of the company they want to invest in. Cash conversion cycle is the amount of time a company takes to convert its resources into cash flows.

Why the Cash Conversion Cycle is so important?

Cash Conversion Cycle is the important Working Capital metric. It helps determine how long it takes for a company’s cash on hand to be converted into inventory and inventory back into cash.

Working Capital comprises of three main components.

1. Inventory

2. Accounts Receivable

3. Accounts Payable

Amazon, Baba, and Apple have negative cash conversion cycle. This is good for business. Why does some business have negative Cash Conversion Cycle?

It is mostly due to the business model. Amazon and Alibaba mostly has third party suppliers for the online orders received from its customers. Amazon receives cash from the customer as soon as the order is placed and it pays its suppliers later.

Apple on the other hand manufactures its own products. The products are expensive and customer usually pays the balance using the credit. In this case, Apple receives the cash right away if it is a third party credit company. If Apple is offering the credit services then it becomes apple's responsibility to collect the payments. However, here the focus is on managing the days of inventory, average collection period and the days of purchase outstanding in order to have negative cash conversion cycle.

Whereas, real estate business has the large cash conversion cycle. This is due to reason that the large inventories/properties are financed by customer pre-sales prior to capital from the bank loan is delivered to the real estate company.

When we look at the Balance sheet and the Income Statement and calculate the Cash Conversion Cycle based on the days inventory, average collection period and the days purchase outstanding.

Now let's look at the sources of data and the related calculations.

Inventory is a working capital on the assets side of the Balance Sheet. This is an important item for business, investors, analysts and customers. It determines the speed with which an item will be delivered to its customers. If you have a product ready it is just the matter of delivery logistics. If it is not ready when the order is placed by the customer, it can significantly delay the order delivery dates and might loose it customers in the long run. On the other hand, holding the inventory for a long time can increase the cost of the inventory due to storage and maintenance and the parts can get obsolete or be a waste over time depending upon the type of inventory. Finance managers have to optimize the inventory as much as possible.

Different types of businesses have different inventory management systems. Depending on whether you are a retailer, a wholesaler or a merchandiser you are likely to have no inventory of raw materials but it is just the finished goods from its supplier in its warehouse. Manufacturing companies on the other hand, have raw materials, in-process goods, and finished goods. Service based industries like Facebook and FedEx have no inventory of any products. Such an account wouldn't exist in their balance sheet.

Inventory is a balance sheet item which indicates the cost of goods sold. The P and L statement takes the COGs and subtracts it from the revenue to determine the gross profit.

The Balance sheet item Inventory and the P/L statement item COGs are related in the following equation.

Inventory at the end of the year = Inventory at the beginning of the Year + Purchases - COGS

Now let's look at some ratios that will will help investors to make investment decisions

Inventory Turnover Ratio = Cost Of Good Sold (COGs)/Average Inventory

A higher inventory turnover represents more efficient inventory management.

Another important ratio related to inventory is, Days Inventory.

Days Inventory = Average Inventory/365

Or

Days Inventory = 365/Inventory Turnover ratio

Days Inventory is closely tied to the inventory turnover. The only difference is that it is expressed as the average number of days the inventory is held before it is sold rather than how many times the inventory turned over during the period.

Cash Conversion Cycle Ratio tells us how long it takes from the time it receives inventory from its suppliers until it receives the cash for the same from the customers. It has a large impact on the cash needs of the business. Having a negative cash conversion cycle is good for business. The business is able to receive cash from the customer before the payment is due to its supplier.

Cash Conversion Cycle = Days Inventory + Average Collection Period - Days Purchases Outstanding

Average Collection Period: The average collection period, sometimes referred to as Days Sales Outstanding or Days Sales in Receivables. Days Purchase Outstanding, we are looking at how long it takes us to pay our vendors. Vendors include suppliers of inventory and also suppliers of services or other non-inventory items

Average Collection Period = Average Accounts Receivable / Credit Sales Per Day

Average Collection Period = 365/Accounts Receivable Turnover

Where:

Accounts Receivable Turnover Ratio = Credit Sales/ Average Accounts Receivables

Days Purchases Outstanding = Average Accounts Payable / (annual credit purchase (or COGs)/365)

Days Purchases Outstanding = 365/Accounts Payable TurnOver

A higher Accounts Receivable turnover represents more efficient cash collections.

Accordingly, the Accounts Payable turnover can be calculated as:

Accounts Payable TurnOver = Credit Purchases (Substitute by COGs when data is not available)/Average Accounts Payable

I hope this information useful to you when you are making the the investment decision.

The is whole another way to look at inventory from the managerial accounting perspective. We will cover that in another post.

Why the Cash Conversion Cycle is so important?

Cash Conversion Cycle is the important Working Capital metric. It helps determine how long it takes for a company’s cash on hand to be converted into inventory and inventory back into cash.

Working Capital comprises of three main components.

1. Inventory

2. Accounts Receivable

3. Accounts Payable

Cash Conversion Cycle = Days Inventory + Average Collection Period - Days Purchases Outstanding

Amazon, Baba, and Apple have negative cash conversion cycle. This is good for business. Why does some business have negative Cash Conversion Cycle?

It is mostly due to the business model. Amazon and Alibaba mostly has third party suppliers for the online orders received from its customers. Amazon receives cash from the customer as soon as the order is placed and it pays its suppliers later.

Apple on the other hand manufactures its own products. The products are expensive and customer usually pays the balance using the credit. In this case, Apple receives the cash right away if it is a third party credit company. If Apple is offering the credit services then it becomes apple's responsibility to collect the payments. However, here the focus is on managing the days of inventory, average collection period and the days of purchase outstanding in order to have negative cash conversion cycle.

Whereas, real estate business has the large cash conversion cycle. This is due to reason that the large inventories/properties are financed by customer pre-sales prior to capital from the bank loan is delivered to the real estate company.

When we look at the Balance sheet and the Income Statement and calculate the Cash Conversion Cycle based on the days inventory, average collection period and the days purchase outstanding.

Now let's look at the sources of data and the related calculations.

Inventory is a working capital on the assets side of the Balance Sheet. This is an important item for business, investors, analysts and customers. It determines the speed with which an item will be delivered to its customers. If you have a product ready it is just the matter of delivery logistics. If it is not ready when the order is placed by the customer, it can significantly delay the order delivery dates and might loose it customers in the long run. On the other hand, holding the inventory for a long time can increase the cost of the inventory due to storage and maintenance and the parts can get obsolete or be a waste over time depending upon the type of inventory. Finance managers have to optimize the inventory as much as possible.

Different types of businesses have different inventory management systems. Depending on whether you are a retailer, a wholesaler or a merchandiser you are likely to have no inventory of raw materials but it is just the finished goods from its supplier in its warehouse. Manufacturing companies on the other hand, have raw materials, in-process goods, and finished goods. Service based industries like Facebook and FedEx have no inventory of any products. Such an account wouldn't exist in their balance sheet.

Inventory is a balance sheet item which indicates the cost of goods sold. The P and L statement takes the COGs and subtracts it from the revenue to determine the gross profit.

The Balance sheet item Inventory and the P/L statement item COGs are related in the following equation.

Inventory at the end of the year = Inventory at the beginning of the Year + Purchases - COGS

Now let's look at some ratios that will will help investors to make investment decisions

Inventory Turnover Ratio = Cost Of Good Sold (COGs)/Average Inventory

A higher inventory turnover represents more efficient inventory management.

Another important ratio related to inventory is, Days Inventory.

Days Inventory = Average Inventory/365

Or

Days Inventory = 365/Inventory Turnover ratio

Days Inventory is closely tied to the inventory turnover. The only difference is that it is expressed as the average number of days the inventory is held before it is sold rather than how many times the inventory turned over during the period.

Cash Conversion Cycle Ratio tells us how long it takes from the time it receives inventory from its suppliers until it receives the cash for the same from the customers. It has a large impact on the cash needs of the business. Having a negative cash conversion cycle is good for business. The business is able to receive cash from the customer before the payment is due to its supplier.

Cash Conversion Cycle = Days Inventory + Average Collection Period - Days Purchases Outstanding

Average Collection Period: The average collection period, sometimes referred to as Days Sales Outstanding or Days Sales in Receivables. Days Purchase Outstanding, we are looking at how long it takes us to pay our vendors. Vendors include suppliers of inventory and also suppliers of services or other non-inventory items

Average Collection Period = Average Accounts Receivable / Credit Sales Per Day

Average Collection Period = 365/Accounts Receivable Turnover

Where:

Accounts Receivable Turnover Ratio = Credit Sales/ Average Accounts Receivables

Days Purchases Outstanding = Average Accounts Payable / (annual credit purchase (or COGs)/365)

Days Purchases Outstanding = 365/Accounts Payable TurnOver

A higher Accounts Receivable turnover represents more efficient cash collections.

Accordingly, the Accounts Payable turnover can be calculated as:

Accounts Payable TurnOver = Credit Purchases (Substitute by COGs when data is not available)/Average Accounts Payable

I hope this information useful to you when you are making the the investment decision.

The is whole another way to look at inventory from the managerial accounting perspective. We will cover that in another post.