Financial Accounting Principals and Guidelines

12/25/2022

Accounting is an information science that is used to collect, analyze, and organize financial data for organizations and individuals. It is quantitative in nature and measures money.

Every firm needs to organize their financial information related to its business. They need to know how much it was able to sell, how much did it cost to produce the product, and how much money it has in the bank. Likewise, Individuals needs to be aware of their personal finances. They need to aware of how much comes in and how much goes out. If the spending is more than earning than they can land into deep trouble. It helps to use and analyze the data from the past to take actions in the present and change the future.

There are four main areas of accounting:

Total Assets - Total Liabilities = Owners Equity

What are assets?

There are many things that could potentially be considered as an asset. While an assist is generally a thing of value, accounting standards provide definitions of what a company can record as an asset on its books.

These standards state that to be considered an asset, an item must:

What are Liabilities?

Liability is an obligation towards others by the company. Generally, a liability must satisfy the following:

What is an Equity?

It is the residual interest in the assets of an entity that remains after deducting its liabilities.

Owners' Equity = Assets - Liabilities

Equity is the resources of the business that belong to its owners. If you add up all of the resources of the business, and subtract all of the claims that third parties have against those assets, what is left for the owners equity.

Businesses record their transactions using direct method or accrual method and prepare their financial reports. They follow the accounting standards and guidelines in reporting and book keeping to share the information with their stakeholders. These standards are vital to uphold the quality, reliability, and consistency the of financial information and assure that the financial statements are comparable from one company to another within the same sector or a different sector.

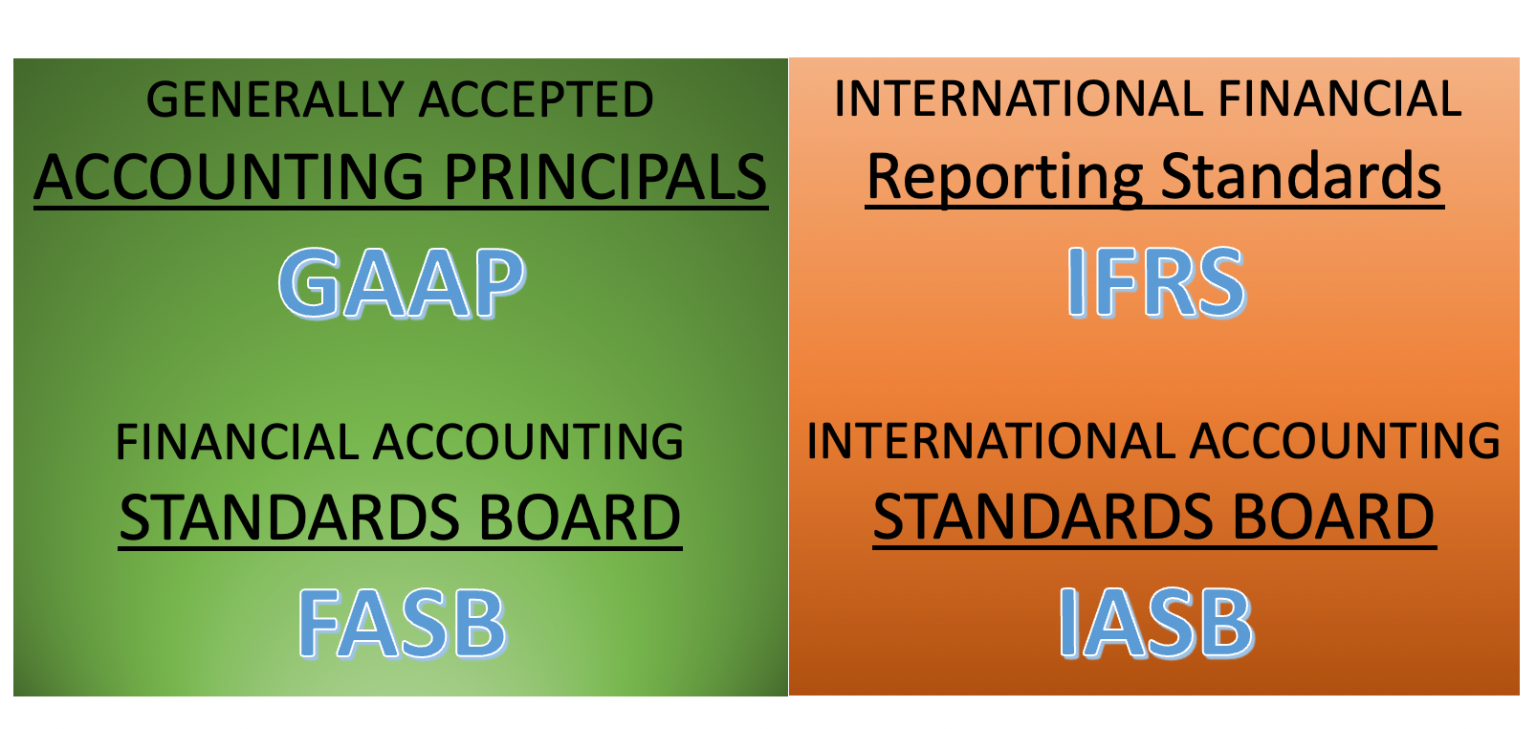

Presently, we have two broad sets of accounting standards: IFRS, used by many countries throughout the world, and US GAAP, which is used primarily within the United States. While the standards are similar in many ways, there are some significant differences. There is significant amount of effort is being taken to create a single accounting standard that will serve the interests of both the groups.

Let's discuss Revenue And Expenses.

Revenue:

According to US FASB, Revenue is, Inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity's ongoing major or central operations.

According to International IASB, The money that an entity receives from providing goods or services to a customer. One important difference, is that the goods or services must be related to the entity's central operations. If a manufacturing company sells a building that it no longer uses, the proceeds received from the sale are not considered revenue as it is not related to the primary function of the business.

There are certain other criteria exist for an entity to be able to recognize revenue under accrual accounting. The business must provided the service or delivered the good to the customer, referred to as earned in accounting, and it must either have received cash from the customer or be confident that the customer will pay, known as realizable in accounting - and in the latter case, it must have an arrangement with the customer that specifies the amount that will be transferred for the good or service.

Expenses

Outflows or incurrence of liabilities from producing goods, rendering services, or carrying out other activities that constitute the firm's ongoing major operations.

It is the costs associated with producing, providing goods or services to a customer.

In terms of accrual accounting, expenses are generally recognized in the period in which the revenues are generated from those expenses.

There are two types of costs the product costs and the period costs. The product costs are related to cost of raw material and any other cost incurred to manufacture the product. This cost should be recorded when revenue from the product is incurred. The examples of period costs are administrative costs, employee salary etc. These costs should also be recorded in the same time period when it is incurred irrespective of the revenue. Recording revenue and costs in the same accounting period is called the matching principle.

Accounting is governed by principles and rules. Some of the guiding principles are conservatism, relevance vs. reliability, historical cost, consistency, materiality, the entity concept, money measurement, and going concern.

Relevance and Reliability: When we mention relevance and reliability, we refer to valid, verifiable, and unbiased data and accounting and reporting practices.

Historical Cost: Follow the accounting principles and guideline to use the historical costs.

Consistency: You need to have consistency in the way you record transactions. Example is depreciations. You cannot change the way you things without having a justifiable reasons. This is known as consistency.

Materiality: Trivial matters don't have to be recorded in the financial reports. We say something is 'material' if it is important. On the other hand something is 'not material' if it is not important. One example of materiality is, "An item if included or accurately informed in a financial report is material if the magnitude of the item is such that it could impact or have the major influence on the decisions made by a person/stakeholder relying upon the report."

Entity: The books of a business are kept separately from the books of individuals, even if there is only one owner of the business. This is called the entity concept in accounting. A business is a distinct, separately identifiable entity. Only transactions of the business entity should be recorded in business account.

Money Measurement: Related to reliability and historical cost. For example, you are the founder of an independent Private Wealth Management Company and your first client gave you good reviews and has also recommended your business in his/her network through word of mouth. You are hopeful that this will help financially but your accountant has not recorded anything related to this good reviews or recommendations in the report. It can sometimes not work as planned and this may lead to setting false expectations for the other investors/clients of the company.

Going Concern: It refers to the fact the business will operate in foreseeable feature. It allows us to accrual accounting. For example, If you say that, VYoga Studio is a, "Going Concern", we mean that it is a business that we expect to continue to operate for the foreseeable future. If you are the owner or investor in the VYoga Studio, this is obviously a good thing. If, on the other hand, a company is, "NOT A Going Concern", then that is something you should worry about.

I hope the accounting principals and guidelines shared above are useful to you as a quick review of accounting concepts as well as a serves as a reminder to refresh and read these concepts in detail to excel in your financial accounting and management profession or hire the right talent to serve your business needs.

Every firm needs to organize their financial information related to its business. They need to know how much it was able to sell, how much did it cost to produce the product, and how much money it has in the bank. Likewise, Individuals needs to be aware of their personal finances. They need to aware of how much comes in and how much goes out. If the spending is more than earning than they can land into deep trouble. It helps to use and analyze the data from the past to take actions in the present and change the future.

There are four main areas of accounting:

- Bookkeeping: It is a fundamental activity to ensure financial information has been gathered systematically.

- Financial Accounting: It focuses on the Income Statement, Balance Sheet and the Cash Flow Statement. These three statements helps to create annual reports. This report is useful to its owners, investors, lenders, financial analysts, and external stakeholders. This makes them comparable across competitors and industries. It provides banks and investors specific information useful in decision making related to sales volume, profitability, and the sources of finances of the firm. The financial statements are created following the set of rules and guidelines. These globally accepted set of rules are called Accounting Principals.

- Managerial Accounting: It is available only for insiders. It is not defined by the accounting principals. It contains strategic information that shouldn't be seen by the firms competitors. It decides on strategies for pricing, completion, marginality, budgeting and other similar topics.

- Tax Accounting: It determines how much taxes a company has to pay. It is very technical field and varies for every legislation in the world.

Total Assets - Total Liabilities = Owners Equity

What are assets?

There are many things that could potentially be considered as an asset. While an assist is generally a thing of value, accounting standards provide definitions of what a company can record as an asset on its books.

These standards state that to be considered an asset, an item must:

- It should purchased at a cost that is measurable

- It should produce probable economic benefit in the future

- It should be owned or controlled by the entity

- It should be result from a past event

What are Liabilities?

Liability is an obligation towards others by the company. Generally, a liability must satisfy the following:

- It must impose a probable economic obligation on economic resources in the future

- The obligation has to be to another entity

- The event that created the obligation must have occurred in the past

What is an Equity?

It is the residual interest in the assets of an entity that remains after deducting its liabilities.

Owners' Equity = Assets - Liabilities

Equity is the resources of the business that belong to its owners. If you add up all of the resources of the business, and subtract all of the claims that third parties have against those assets, what is left for the owners equity.

Businesses record their transactions using direct method or accrual method and prepare their financial reports. They follow the accounting standards and guidelines in reporting and book keeping to share the information with their stakeholders. These standards are vital to uphold the quality, reliability, and consistency the of financial information and assure that the financial statements are comparable from one company to another within the same sector or a different sector.

Presently, we have two broad sets of accounting standards: IFRS, used by many countries throughout the world, and US GAAP, which is used primarily within the United States. While the standards are similar in many ways, there are some significant differences. There is significant amount of effort is being taken to create a single accounting standard that will serve the interests of both the groups.

Let's discuss Revenue And Expenses.

Revenue:

According to US FASB, Revenue is, Inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity's ongoing major or central operations.

According to International IASB, The money that an entity receives from providing goods or services to a customer. One important difference, is that the goods or services must be related to the entity's central operations. If a manufacturing company sells a building that it no longer uses, the proceeds received from the sale are not considered revenue as it is not related to the primary function of the business.

There are certain other criteria exist for an entity to be able to recognize revenue under accrual accounting. The business must provided the service or delivered the good to the customer, referred to as earned in accounting, and it must either have received cash from the customer or be confident that the customer will pay, known as realizable in accounting - and in the latter case, it must have an arrangement with the customer that specifies the amount that will be transferred for the good or service.

Expenses

Outflows or incurrence of liabilities from producing goods, rendering services, or carrying out other activities that constitute the firm's ongoing major operations.

It is the costs associated with producing, providing goods or services to a customer.

In terms of accrual accounting, expenses are generally recognized in the period in which the revenues are generated from those expenses.

There are two types of costs the product costs and the period costs. The product costs are related to cost of raw material and any other cost incurred to manufacture the product. This cost should be recorded when revenue from the product is incurred. The examples of period costs are administrative costs, employee salary etc. These costs should also be recorded in the same time period when it is incurred irrespective of the revenue. Recording revenue and costs in the same accounting period is called the matching principle.

Accounting is governed by principles and rules. Some of the guiding principles are conservatism, relevance vs. reliability, historical cost, consistency, materiality, the entity concept, money measurement, and going concern.

Relevance and Reliability: When we mention relevance and reliability, we refer to valid, verifiable, and unbiased data and accounting and reporting practices.

Historical Cost: Follow the accounting principles and guideline to use the historical costs.

Consistency: You need to have consistency in the way you record transactions. Example is depreciations. You cannot change the way you things without having a justifiable reasons. This is known as consistency.

Materiality: Trivial matters don't have to be recorded in the financial reports. We say something is 'material' if it is important. On the other hand something is 'not material' if it is not important. One example of materiality is, "An item if included or accurately informed in a financial report is material if the magnitude of the item is such that it could impact or have the major influence on the decisions made by a person/stakeholder relying upon the report."

Entity: The books of a business are kept separately from the books of individuals, even if there is only one owner of the business. This is called the entity concept in accounting. A business is a distinct, separately identifiable entity. Only transactions of the business entity should be recorded in business account.

Money Measurement: Related to reliability and historical cost. For example, you are the founder of an independent Private Wealth Management Company and your first client gave you good reviews and has also recommended your business in his/her network through word of mouth. You are hopeful that this will help financially but your accountant has not recorded anything related to this good reviews or recommendations in the report. It can sometimes not work as planned and this may lead to setting false expectations for the other investors/clients of the company.

Going Concern: It refers to the fact the business will operate in foreseeable feature. It allows us to accrual accounting. For example, If you say that, VYoga Studio is a, "Going Concern", we mean that it is a business that we expect to continue to operate for the foreseeable future. If you are the owner or investor in the VYoga Studio, this is obviously a good thing. If, on the other hand, a company is, "NOT A Going Concern", then that is something you should worry about.

I hope the accounting principals and guidelines shared above are useful to you as a quick review of accounting concepts as well as a serves as a reminder to refresh and read these concepts in detail to excel in your financial accounting and management profession or hire the right talent to serve your business needs.